This “gigantic, fabulous debt,” Macaulay went on, “was considered, not merely by the rude multitude, not merely by fox-hunting squires and coffee-house orators, but by acute and profound thinkers, as an incumbrance which would permanently cripple the body politic.”

Apparently, each generation must rediscover what seems at the time an heretical idea: debt prudently incurred and productively employed, can benefit a nation; and having made that discovery, each generation must relearn how to discern between prudence and profligacy. Each generation must forge a new synthesis between the anti-debt canons of fiscal integrity handed down to it from earlier generations and the antithetical financial innovations of contemporary financiers and entrepreneurs.

The reason, we think, is clear. Debt and the risk-taking associated with it are the nuclear forces of economics. Financial leverage is an incredibly powerful source of economic energy. Properly harnessed, debt can fuel a business and an entire economy to unprecedented heights of success and prosperity. Imprudently handled, it can lead to economic meltdown.

It is not surprising that citizens worry at the prospect of politicians free to manage either nuclear power or public borrowing. However, as rolling electricity blackouts in California and the slowing world economy demonstrate, “eco-extremism”—whether economic or ecological—stifles supply and invites decline.

Writing from the left, Robert Heilbroner and Peter Bernstein said it best in The Debt and the Deficit: False Alarms/Real Possibilities, as deficit hysteria peaked and the Reagan administration ended:

“ It is certainly possible to amass a debt that will cripple this country or to run up deficits that would plunge us into economic chaos, but there is nothing in the immediate situation to warrant such imaginings…Even in the absence of [Reagan’s] tax cuts or any military buildup, we would still have faced the extraordinary problem of an exploding deficit because of inflation-swollen entitlements, inflation-boosted interest rates, and post-inflation reduced tax revenues…In normal times we favor a ‘deficit,’ by which we mean growth-promoting expenditures…of 2 to 3 percent of GNP.” ii

From the right, George Gilder said it best in Wealth and Poverty:

“ Debt that is wantonly monetized or accompanied by chaos . . .or debt that is prodigally incurred,…can bring ruin. Debt…which is piled up to finance programs paying people not to work; combined with penalties on business for being profitable, can destroy an economy. But debt that is incurred for capital projects of benefit to citizens and their productivity, or debt that is incurred to avoid inflicting destructive taxes on growing firms — such liabilities can become vital assets of growth and progress. The worst economic disaster is to blight the future by suppressing the catalytic ventures on the economic frontiers.” iii

And about surpluses, no one said it better than Ronald Reagan:

“ I have always believed that government has no right to a surplus; that it should take from the people only the amount necessary to fund government’s legitimate functions. If it takes more than enough it should return the surplus to the people.” iv

Introduction

In 1997, budget deficits turned into budget surpluses as far as the eye could see—that is, for the next 10 to 15 years. Simultaneously, a counterproductive Washington Consensus emerged on the banks of the Potomac: politicians on both sides of the political aisle decided that the best use of the surpluses was to pay down the debt by letting the surpluses run. Ostensibly, the consensus rested on economic considerations; actually, it arose from a partisan stalemate of convenience. The Washington Stalemate now in place uses budget surpluses as a wedge between tax revenue and government spending, blocking tax cuts on one side and spending increases on the other. The consensus is one of politics, not economics.

Federal Reserve Board Chairman Alan Greenspan, however, recently revealed a small crack in that consensus. He said that rushing to retire the national debt is not the best fiscal policy for America, and he raised two concerns with allowing huge budget surpluses to run indefinitely.

First, he warned that projected surpluses are now so large they will outrun the total outstanding federal debt held by the public before the end of the decade.1 From that point forward, the federal government would have to use the surpluses to purchase large quantities of private assets, a course he strongly advised against.2 Rightly so; government accumulation of private sector assets is precisely the opposite of privatization; it is socialism.3

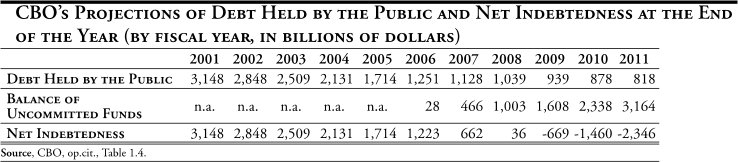

Second, Chairman Greenspan warned that those undesirable conditions would begin well before every dollar of outstanding debt could be retired.4 According to Congressional Budget Office (CBO) projections, between 2008 and 2011 the federal government could accumulate surpluses of $3.2 trillion for which there would be no federal debt to retire. [See Appendix Table A-1] With no maturing T-bonds to retire at face value, the government would have to pay market value, which would bid up bond prices. In its Fiscal Year 2002 budget, the Bush Administration estimates that to retire the remaining outstanding debt before maturity would cost $50 to $150 billion because bond holders would demand bonus payments as enticements to redeem their bonds early, a course the administration calls “wasteful and senseless.”5

As an alternative to spending the “excess” surpluses on non-Social Security programs or using the accumulating surpluses to purchase private assets, Chairman Greenspan supported modest tax cuts and suggested that remaining surpluses not devoted to debt retirement might be placed in private retirement accounts.6

These special circumstances aside, Mr. Greenspan continued to express the curious conviction that:

“ All else being equal, a declining level of federal debt is desirable because it holds down long-term real interest rates, thereby lowering the cost of capital and elevating private investment. The rapid capital deepening that has occurred in the U.S. economy in recent years is a testament to these benefits.”7

Thus, even as the Fed Chairman suggested that the Washington Stalemate be broken in favor of cutting tax rates, he maintained his long-time endorsement of a budgetary strategy that creates a “glide path to zero federal debt or, more realistically, to the level of federal debt that is an effective irreducible minimum.” In a later Capitol Hill appearance, Greenspan went further and warned of detrimental economic consequences if tax cuts were used to prevent the government’s accumulation of assets.8 This argument rests on shaky ground. It assumes that debt reduction favorably affects interest rates, saving and productivity growth—assertions we question.

This paper rejects the conventional wisdom that we should retire the national debt to “an effective irreducible minimum” as soon as possible. We seek to demonstrate that America at the dawn of the 21st century should stabilize the debt burden right where it is, at about one-third of national income. This “debt-burden neutral” fiscal strategy would allow the federal government to borrow additional funds each year sufficient to overhaul the tax code and to convert Social Security into a payroll-tax-financed, worker-investment retirement program.

The thesis of this paper is that borrowing prudently to create a new tax code and a new investment-based retirement program will produce steady and long-term growth, greater security and a higher standard of living than would paying off the debt and accumulating a large portfolio of private assets. The long-term steady course we recommend would control borrowing to safe, sustainable levels indefinitely into the future. By contrast, the short-term crash course to pay off the debt would bequeath uncontrollable borrowing, unbearable tax increases and unacceptable retirement benefit reductions to future generations— beginning with baby boomers—in order to preserve the pay-as-you-go Social Security system. We strongly favor the long-term steady course that holds tax rates to an absolute minimum and maintains borrowing at safe, productive and sustainable levels.

We intend and hope that this paper will help convince policy makers that rushing to retire debt is myopic because it comes at the expense of other more beneficial endeavors, slows our nation’s forward momentum and may even now be tugging America backwards. We also hope that the paper will help policy makers who are open-minded to gather evidence that will enable them to convince their colleagues to choose growth over austerity.

If we can break the Washington Stalemate, our nation can return to a high-growth trajectory that promises everyone a chance to build wealth and realize their version of the American Dream. If we cannot, the nation will have lost its best chance for multi-generational economic health and lasting prosperity.

The Problem

Complex economic choices have been boiled down to oversimplified, destructive sound bites, in an unfortunate violation of Einstein’s warning: “ Everything should be as simple as possible, but not simpler.”

Republicans oppose the expansion of big government—though presumably not national defense enhancement and Social Security repair. Democrats oppose “ ;tax cuts for the rich”—though presumably not for the innovators who create new jobs, products and services when they are freed from oppressive taxes and regulations. But the sound bites get the headlines, and the exceptions get lost.

Sadly, it is sound-bite politics that led to the stalemate described above. “Debt reduction” is an effective sound bite, and both sides love it. The Democrats have settled on it as the way to block Republican tax cuts, and the Republicans have chosen it as the way to block Democratic spending increases. Both positions are based on the false premise that reducing the nominal dollar level of debt through fiscal austerity is sound financial practice—a premise disproved every day by successful private sector firms and by our nation’s economic track record. And that false premise now threatens the vibrant economy we should bequeath to future generations.

A Three-Step Recovery Program: Transcending Fear of Prudent Financial Leverage

Step 1: Admit that the private sector drives economic growth and that it responds to economic incentives at the margin. Acknowledge that raising the after-tax rate of return to working, saving and investing will increase all three, which will invigorate productivity growth, the key to sustained economic expansion. Concede the capitalist principle that prudent use of financial leverage enhances the process of wealth creation and can continue to work for our nation, just as it does for firms and individuals.

Step 2: Trust the market. Trust the private sector to deliver when participants have the incentives to do so. It worked in the 1960s under President Kennedy and again in the 1980s under President Reagan. It also worked under President Clinton and the Republican Congress after they cut capital gains tax rates, introduced Roth IRAs, opened markets, reformed welfare and freed the new economy from some stifling regulations. The market process that has made the United States of America the wealthiest nation in history can continue doing so in the 21st century.

Step 3: Enjoy the fruits of increased economic growth:

- Higher incomes and living standards for all,

- Lower tax burden for the private sector,

- Larger tax base from the growing private sector,

- Safe, steady and manageable level of debt (financial leverage), and

- Larger subsequent tax revenues to support such essential federal programs as modernized national defense and revitalized Social Security.

The rest of this paper covers the entire topic, from problem to solution, in detail.

Lessons From the Past

Lessons from the Founding: Hamilton v. Jefferson

Vigorous argument over budget deficits and the national debt in America dates from the seminal debate between Alexander Hamilton and Thomas Jefferson. Hamilton saw value in using the nation’s borrowing power to establish and maintain a rock-solid currency, which he believed would permit the young United States to become an economic powerhouse. “If it is not excessive,” Hamilton declared, “a national debt will be to us a national blessing.”

Jefferson at first disagreed: “Loading up the nation with debt and leaving it for the following generations to pay is morally irresponsible. No nation has a right to contract debt for periods longer than the majority contracting it can expect to live.” A decade later, reflecting back on the new Constitution, Jefferson wrote that if he could obtain one constitutional amendment he would remove the federal government’s power to borrow. However, five years later as president, Jefferson reversed his opinion. For $15 million, most of which was borrowed, he bought the Louisiana Territory from France. That single transaction was one of the best investments in our nation’s history, even though it caused the national debt to skyrocket from $77.1 million to $86.4 million (a 12 percent increase in one year). Jefferson’s decisive action, universally and correctly praised, was also a de facto admission that Hamilton had been correct. The ability to make prudent use of the nation’s borrowing power was and still is a national blessing.

Lessons from the Recent Past

Twenty years ago, America once again experienced the virtues of prudently using debt to achieve a great national purpose, this time economic revival. In 1980, the country was mired in “stagflation”—simultaneously accelerating inflation and rising unemployment. The economy had jumped off the Phillips Curve into unknown territory.9 Conventional economic theory had reached a dead end; its remedy for reducing unemployment was the opposite of its remedy for reducing inflation.

Some economists threw up their hands and counseled resorting to wage and price controls; most others wagged their fingers and recommended raising tax rates (to dampen inflation) and printing more money (to stimulate aggregate demand)—the economic equivalent of stepping on the brake and the accelerator at the same time. The economy overheats but doesn’t go anywhere.

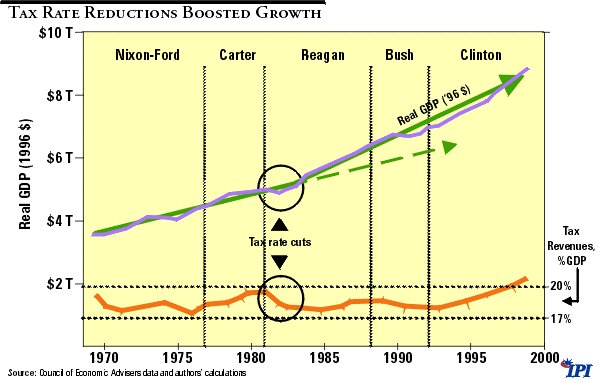

Ronald Reagan found a solution to the stagflation paradox. Rejecting the prevailing opinion that aggregate demand drives economic expansion, President Reagan recognized the need to restore economic incentives. He devised an economic program that (1) cut tax rates across the board to raise the after-tax rate of return to work, saving and investment, (2) promoted sound money to prevent an erosion of wealth, the reward for hard work and sound investment and (3) reduced excessive regulation on workers, savers, investors, businesses and entrepreneurs.

The key to Reagan’s economic strategy was his understanding that when tax rates are too high, the financial and business decisions people make at the margin—that is, on the next dollar earned, spent, saved or invested— are based more on tax considerations than on economic considerations. In that respect, Reagan’s policies coincided with John Maynard Keynes’ assertion that no one should have to pay a tax rate higher than 25 percent during peacetime. But Reagan also asserted that proper spending priorities would serve to maintain the peace, thereby allowing the economy to grow uninterrupted by the ravages of war and permitting tax rates to remain low indefinitely.

Figure 1

Keynes’ maxim on tax rates recognizes a fundamental truth that too many subsequent economists forgot: people work, save and invest for after-tax income and return. In the General Theory, Keynes wrote, “Income taxes, especially when they discriminate against ‘unearned’ income, taxes on capital profits, death duties and the like are as relevant as the rate of interest.”10 When tax rates rise, they reduce the after-tax return to working, saving and investing, and people do less of all three. Lower tax rates increase the after-tax rate of return and encourage people to engage in more productive activities. The key to understanding the Archimedean power of the pro-growth strategy is appreciating the enormous leverage created when the after-tax rate of return rises. It is like a call-to-arms for all the factors of production, as every productive force in the economy immediately responds so as to take advantage of new opportunities.

The crippling effect of high tax rates is particularly pronounced under a regime of progressive taxation, and it is compounded when inflation is added: as people’s incomes rise, even if only because of inflation, they are propelled upward through ever higher tax brackets. The economy grows more slowly under the burden of higher tax rates, and less revenue flows into government coffers.

Empirical evidence indicates that once tax rates rise above about 20 percent, reductions in the after-tax rate of return on productive activities begin to significantly affect economic behavior and erode economic performance.11 Not only is the economy deprived of the full measure of labor and capital it requires to grow at or near its capacity, the government is deprived of revenue as the tax base and therefore tax receipts fall. Moreover, if tax rates are left high enough long enough, as Nobel Prize winning economist Robert Mundell has pointed out, they asphyxiate the economy by depriving it of the oxygen of labor and capital it requires.

President Reagan’s pro-growth strategy worked. Except for a short economic downturn in 1990–91 during the first Bush administration and a slow recovery during President Clinton’s first term—both brought on by tax rate increases, new regulations and “stop-go” monetary policy— America has enjoyed 18 years of falling or stable inflation and fast-paced, uninterrupted economic expansion.

Despite the success of the Reagan administration’s pro-growth policies, the political-economic paradigm in today’s Washington, D.C. is austerity masquerading as fiscal discipline. What really is going on requires some explanation.

Historic Roots of the Contemporary Debate

The contemporary debate in Washington over budget deficits and the national debt has been less noble and more theatrical than that between Hamilton and Jefferson. In large part, that is because public borrowings have not in recent years been applied to solid investments of great national purpose.

In 1970, Richard Nixon is said to have quipped, “We are all Keynesians now.” As president, he based a major expansion of the federal government on principles that embraced high progressive tax rates and the aggressive use of public borrowing as a political-economic management tool and means of redistributing income. At that point, Republicans essentially abandoned any moral objections to deficits—objections they may have inherited from Jefferson. Nevertheless, a potent strain of Hooverite austerity lingered on within the GOP. That austerity mentality dated back to President Hoover’s insistence on raising tax rates and balancing the budget to fight an economic contraction, which ironically helped cause the Great Depression.

In recent times, the political opposition to deficits and the public debt has been based more on political expediency than on moral or economic principles. After the dramatic expansion of government by presidents Johnson and Nixon, Republicans found it expedient to rail against budget deficits—an argument to which they found the public generally receptive—when, in fact, the object of their ire and opposition was rising federal spending. Getting spending under control was a hard sell to a public accustomed to the redistribution programs of the 1960s and 1970s.

By the 1980s, most Republicans placed the blame for expanding, redistributive government on deficit spending. The belief that deficits fueled the growth of the welfare state, more than a fear that the public debt was out of control, accounted for conservatives’ opposition to deficits. They believed it would be more difficult for liberals to increase spending if Congress were forced to balance the books each year. As a result, many conservatives began favoring a balanced budget/tax limitation amendment to the U.S. Constitution.

Jack Kemp, long an advocate of pro-growth strategies, refused to become obsessed with debt and deficit avoidance policies because of their growth-stifling implications. He put it this way in a 1985 speech to the Economic Club of Detroit:

While deficits do matter, they matter as a symptom of a deep problem—the problem is that our economy has fallen below its potential for the last decade or so while government spending and taxes have ballooned. If we can enact fundamental economic policies to insure sustained non-inflationary economic growth and reduce government spending, then the solution to our deficit problem will be in sight.

Reaganomics & Clintonomics

In 1981, President Reagan defied the Republican taboo against enlarging the public debt and sidestepped the Hoover wing of the Republican Party. He shed the GOP inhibitions against deficits to enact a program for economic revival even though the congressional leadership of his own party characterized his program as a “river boat gamble,” and his own budget director called it a Trojan horse to dismantle the welfare state. In Reagan’s framework, current-period deficits were considered an investment in tax rate reductions that would boost the nation’s wealth creating capacity.12 The investment has paid off handsomely. Companies and industries incubated in the Reagan years have become the world’s engines of growth.

Ronald Reagan, like Thomas Jefferson, saw the great public purpose to be achieved by prudent use of the country’s borrowing power. He implemented his programs in spite of then-record budget deficits that leaders of both political parties erroneously blamed on the Reagan tax rate cuts. The deficits were the opposite of failed policy outcomes; they were successful investments in national security and long-term economic growth.

Collapsing inflation contributed to the Reagan deficits by halting bracket-creep-driven revenue growth, which had been keeping the Treasury awash in revenue. Spending growth did not collapse in tandem with revenues as inflation fell, but instead accelerated to match the path that revenues would have taken if they had continued to be driven skyward by inflation. To the extent that the tax rate reductions produced a one-time reduction in the revenue base, they accounted for about 10 percent of the deficits; new spending accounted for the remainder.13 Although Reagan preferred to eliminate wasteful and unproductive spending, when blocked from doing so by the Democratic Congress he accepted the resulting deficits rather than subordinate national security priorities or curtail tax rate reductions.

In other words, the Reagan tax rate reduction cannot legitimately be blamed for anything but instead deserves credit for improving the economy. The economic growth has continued; the budget deficits were transitory. As a percent of GDP, the deficit was virtually the same the day Ronald Reagan left the White House (2.8 percent) as the day he entered it (2.7 percent).

Democrats who for years had been under the illusion that budget deficits provided desirable economic stimulus, found “fiscal discipline” in the 1980s, seizing upon it as a political strategy for denouncing Reagan administration policies. After Reagan’s steep, across-the-board tax rate reductions, his political opponents sought to frame the federal deficit and public debt as problems and then blame them on the rate reductions. The profligacy frame was convenient because so many Republicans were apologetic about the deficits and found it impossible to overcome the debt phobia they had suffered throughout their political careers.

The result of the bipartisan cabal against deficits was almost yearly tax increases between 1982 and 1986. Jack Kemp, however, remained unapologetic for the Reagan/Kemp/Roth tax rate reductions and in 1988 exposed the Achilles heel of the conservative movement: “Conservatives have often been more successful in changing prevailing political rhetoric than in changing policy. And with establishment Republicans, the new rhetoric is not matched by a determination to put it into action.” He also exposed the Democrats’ newfound fiscal discipline for what it was: “In the Democratic Party,” ; Kemp said, “‘fiscal discipline’ has become a new code name for tax increases.”14

Debt phobia was doubly ironic for the Republicans. They were supposed to be quintessential capitalists, willing and able to use financial leverage prudently to enhance growth, who found themselves paralyzed by debt phobia. That led to the 1990 tax hike which contributed to the recession and in turn handed the presidential election of 1992 to Bill Clinton.

By the end of President Clinton’s second term, austerity economics had infected his administration too. Clinton and members of his administration sounded more like Herbert Hoover than Hoover himself. In May 2000, for example, Treasury Secretary Lawrence Summers articulated debt retirement as the organizing principle of the Clinton administration’s economic policy when he told reporters that “a strategy based on debt reduction with appropriate accompanying policies is, in all of our judgment, the strategy that maximizes the prospects for continued prosperity, both now and in the future.”

Summers’s statement was a natural extension of the oft-repeated Clintonomics assertion that “deficit reduction helped the economy grow”—a superb example of cause-effect reversal. In fact, it had been a growing economy that caused deficits to shrink, precisely as George Gilder had predicted shortly after Clinton took office. In March 1993, Gilder said, ”[President Clinton will be] the beneficiary of just the most explosive advance in technology in the history of the human race… it could engulf his Administration with prosperity in a way that would render most of his adverse policies almost irrelevant." How right Gilder was.

In many respects then, Clinton was a product of the Washington Stalemate and the tense political equilibrium that settled over the nation’s capital in the early 1990s when the austerity wing of the GOP regained ascendancy. A partisan stalemate arose between Republicans who opposed spending increases and expansion of redistributive government and Democrats who opposed broad tax rate reductions and contraction of government. In other words, both parties’ fierce opposition to deficits and expanding the national debt arose as a blocking strategy, based on a belief that government borrowing would facilitate the achievement of their rival’s purpose. Ironically, this defensive posture led the two sides to cooperate in enacting the so-called pay-go rules that would maintain the stalemate. When surprising growth-driven surpluses emerged in 1998, debt retirement became the consensus option by default.

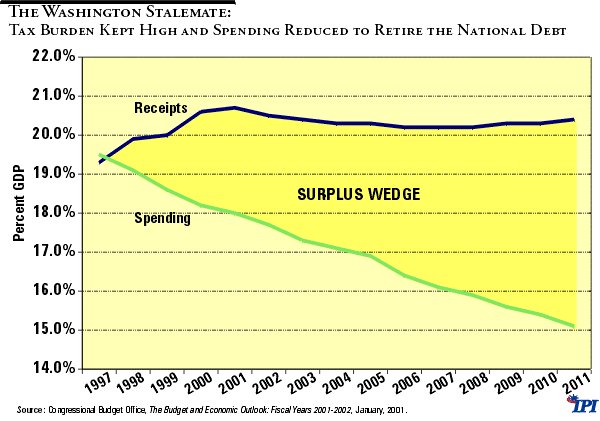

The Battle of the Wedge

As a result of the Washington Stalemate and a rapidly growing economy, budget surpluses of $5.6 trillion are anticipated during the coming decade—to be followed by a sudden, dramatic reversal when the baby boomers begin to retire. 15 Both sides of today’s stalemate seem to have achieved their objective, as Figure 2 indicates.

Figure 2

In 2000, the federal tax burden as a share of GDP rose to 20.6 percent, coming to within 0.3 percent of its all time high of 1944. As 2001 began, revenues were slated to stay near this record level indefinitely into the future. Federal spending has fallen below 18 percent of GDP for the first time since 1966 and is expected to fall to 15.1 percent in 2011, the lowest since 1949. The area between these two lines represents the surplus wedge over which the political battles now rage.

Both sides must now grapple with large federal surpluses projected to last for a dozen years. Both sides fear that breaking the stalemate will advantage their opponents. Meanwhile, the economy and the most productive citizens suffer.

Over the long run, this equilibrium will prove ephemeral. Both Republican and Democratic members of Congress have begun using the surpluses to leverage nonfundamental spending up again, and time is on their side.16 Although it is conceivable that Congress will continue to reduce tax rates to bring the budget into balance at the lower spending level, it is more likely that the Stalemate will prevent significant additional tax rate reductions and the surpluses will disappear into higher spending increases.

Even with the Bush tax cuts now enacted into law, revenues are projected to remain at or above 18 percent of GDP for the next decade. Having compromised slightly on tax rates and bemoaned a return to fiscal profligacy, while actually giving little ground in the struggle for the surplus wedge, tax-cut opponents are strategically positioned to block further rate cuts and to increase the pressure for more spending. Indeed, spending already has begun to encroach on the surplus wedge as evidenced by President Bush’s 2002 budget initiative to create a $1 trillion fund, the only purpose of which is to “ ;meet other programmatic and contingency needs as they arise.”17

If government is to be confined to its fundamental duties, which is perfectly achievable on the spending path the CBO currently projects, the public must be rallied around great national purposes such as fundamental tax reform and privatization of Social Security to protect future retirees. Not only would these two projects absorb all surpluses, but they also would require prudent mobilization of the nation’s borrowing capacity and foreclose expansion of government into nonfundamental areas. George W. Bush’s tax cut proposals and 2002 budget are the first administrative directives in the Battle of the Wedge. With Democrats now in control of the Senate, a counter offensive on spending can be expected any time now.

The Debt-Retirement Fallacy

Debt Is a Financial Tool

Debt is intrinsically neither good nor bad. Debt is simply a financial tool and like any other tool can be either productive or dangerous. Cathy Matson of the University of Delaware brings the controversy over the public debt into focus in her review of John Steele Gordon’s concise history of the national debt, Hamilton’s Blessing: The Extraordinary Life and Times of Our National Debt:

Gordon’s sustaining point is that we must relearn what Hamilton knew: the size of the debt is not itself a problem, but the sloppy hodgepodge of policies regarding taxing and spending that have accumulated over generations without fiscal planning threatens the body politic. It is not the presence of a national debt, but the uses to which it is put for the sake of political expediency, Gordon insists, that endanger the national interest.18

A visionary use of public debt at the start of the 21st century would be to completely overhaul the federal tax system and fundamentally restructure Social Security as a personal investment program.

New borrowing is necessary to achieving this vision because two formidable political obstacles stand in the way:

- The political and moral requirement to hold people harmless who have made life-defining and business-defining decisions based on the current tax code, which cannot be accomplished under a “revenue neutrality” constraint; and

- The political and moral requirement to guarantee all current retirees and workers the full retirement benefits they have been promised while simultaneously diverting a significant share of the payroll tax into personal retirement accounts.

A “debt-burden neutral” fiscal policy is safe, achievable and vital. Prudent, controlled borrowing, undertaken now to overhaul the tax code and restructure Social Security, will yield a future windfall of higher revenues from a larger tax base at lower rates—which in turn will fend off unavoidable, uncontrollable borrowing when the boomers retire.

Myths about the National Debt

Over the years, politicians have latched onto a variety of myths regarding government debt and deficits. In repeating the myths, many politicians have come to believe them.

An obsession with debt retirement is a product of a single-entry bookkeeping mentality and what philosophers of science call the “composition” fallacy, i.e., erroneously applying to groups truths that hold only for individuals.

In evaluating the best government policy toward debt and taxes, policy makers commit the composition fallacy most frequently by failing to recognize the critical distinction between governments and individuals. Individuals eventually retire and die and the entrepreneurial ventures, partnerships and sole proprietorships they create have a high probability of forced liquidation even during their lifetime; therefore, debt elimination is a common goal for individuals. Successful corporations, on the other hand, are far more likely to continue in spite of the deaths of individual employees or owners, in spite of economic downturns and in spite of short-term cash flow difficulties. As a result, debt rollover is a viable financial option.

Lastly, the United States government is virtually certain to continue on even longer than the healthiest of corporations. Markets evaluate its financial status accordingly, which permits the federal government to roll its debt over, borrow to supplement tax revenues, and pay interest on its debt in perpetuity—without paying an interest rate premium or having to retire principal. It is a financial privilege to which few people or businesses could aspire. U.S. Treasury bonds are safe, sound, solid and highly respected worldwide. They are in fact the very basis of our money.

Debt Retirement Does Not Eliminate the Interest Burden

The most important lesson many in Washington fail to grasp is that the interest burden of borrowing cannot be eliminated simply by retiring debt. The obsession over the amount of interest due on the public debt (approximately $3,450 billion between 2000 and 2015), fails to take into account the growth-inducing private investment opportunities that would have to be taxed away ($3,639 billion) in order to retire the public debt and eliminate those interest payments. To repeat, retiring outstanding debt does not eliminate the interest burden of borrowing; nothing short of default can do that, and default, of course, creates an entirely new set of financial burdens.

The interest burden of borrowing is incurred at the time borrowing occurs and must be borne in either of two ways: (1) directly at each future time period in which interest is paid or (2) indirectly as an opportunity cost by retiring the outstanding principal all at once. In the latter case, the burden comprises the foregone return on the investment that would have come from the monies used to retire the debt. The present value is identical in either case, and it is the investment return on alternative uses of available money that determines which of the two options is preferable.

Said another way, it is sound financial practice for the government to borrow money at 6 percent interest, then invest it for a 10 percent return. But debt retirement eliminates that choice. By refusing to borrow at 6 percent, the 10 percent investment opportunity is lost.

Average annual debt service on the federal debt held by the public is now about 6.3 percent. The average rate of return on investment is considerably higher in the private sector than what is achievable through additional government spending programs. Over the long run, mutual funds earn average rates of return in excess of 10 percent. Thus, private investment by the taxpayers of their own money now being hoarded as surpluses in Washington, D.C. would be more productive than using that money to retire the national debt.

Rolling over the debt is perfectly sound financial practice for any entity that’s growing wealthier and wealthier; moreover, prudent use of debt financing can and does enhance long-run growth. Successful corporations do it all the time; so can the nation.19

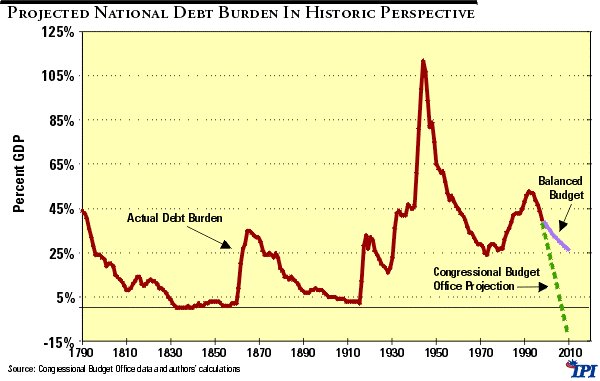

Nation’s Capacity to Service Debt Is Overlooked

Policy makers also obsess over the size of the public debt ($3.4 trillion) without considering the nation’s income producing capacity to service that debt. Over America’s entire history, with only brief periods of economic contraction, the nation’s output has grown steadily. Over the past 50 years, GDP has grown at an average annual rate of 3.2 percent after accounting for inflation. In 2000, GDP stood at $10 trillion, and with the right economic policies, it can be expected to grow at least as fast and probably faster indefinitely into the future.

Figure 3

Policy makers miss the fact that although the debt held by the public rose by more than 50 percent from 1990 to 2000 (from $2,410 billion to $3,639 billion), the debt burden on the economy fell from 42.4 percent of GDP to 36.2 percent because the economy grew faster than the debt. If the federal budget remains in balance, surpluses are returned to taxpayers through tax rate reductions and the economy grows during the next 15 years no faster than it has on average throughout the post World War II era (3.2 percent a year), the debt burden on the economy will fall to less than 15 percent of GDP by 2015 without a single dollar of debt having been retired.

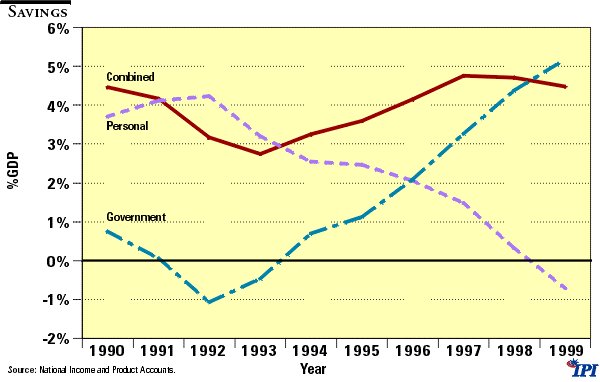

Debt Retirement Does Not Increase Saving

The argument for reducing government debt to spur private sector economic growth is that government debt retirement increases national saving. That is unlikely. In fact, contemporary experience suggests just the opposite. Since 1993, during which time deficits turned into surpluses, budget surpluses have come almost directly at the expense of lower personal saving.

Figure 4

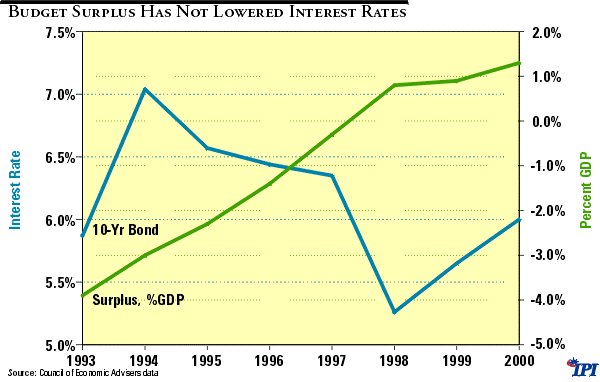

Deficit/Debt Reduction Has Not Lowered Interest Rates

From this false premise, debt phobia has led to a false conclusion. Policy makers of both parties make extravagant but unsubstantiated claims about how debt retirement will strengthen the economy by lowering interest rates. The weight of the empirical evidence is that interest rates were unaffected by government budget deficits even when they hit their highest point in recent times, 6.1 percent of GDP in 1983.

Figure 5

It is little wonder interest rates are unaffected by budget deficits. That 6.1 percent of GDP would amount to about $600 billion today, or a mere 0.8 percent of the $70 trillion global capital market. In today’s global economy, interest rates are determined by the combined effects of inflation, inflation expectations and the prevailing real rate of return to capital, which in no small part is determined by government tax and regulatory policies.

Since there is no credible evidence that the current level of outstanding government debt raises interest rates by so much as a single basis point in the United States, there should be no expectation that retiring the debt would lower interest rates. Again, current experience illustrates this proposition. Since 1993, interest rates in general have risen, not fallen.

How to Escape the Austerity Trap

The theme of this paper is that a prudent, growth-oriented policy would yield better overall economic performance and faster living standard increases for all Americans. To enjoy those benefits, we must first get out of the debt phobia box.

This section will suggest a means of escape.

The choices we face for financing federal expenditures have a clear analogy in private sector business. We will draw on that analogy to explain what’s right and wrong with each of the following four choices for fiscal policy:

- Debt Retirement

- Balanced Budget

- Debt-Burden Neutrality

- Growing Debt Burden

Under current circumstances, we favor 3, the Debt Burden Neutrality policy, because it is the least risky, most lucrative way to maximize the wealth and well-being of future generations. We explain each of the four choices below, but first we offer some background on the business sector analogy we use to explain each public policy choice.

Growth Leverage: A Private Sector Business Analogy

As we showed earlier, to draw analogies between government and individual debt too quickly can be misleading. However, comparing the way private business and the government plan their budgets can be instructive. Both budget for future spending—usually next year’s spending. Also, both spend money two ways: (1) for current operations and (2) for capital expenses expected to yield wealth-enhancing benefits beyond the current budget year.

The difference in how government and business account for those two ways of spending is also important. Business keeps operating expenses separated from capital expenditures; government essentially does not. As any banker can attest, borrowing heavily just to keep current operations afloat is unwise, but prudent borrowing to help fund promising investments is sound financial practice. Businesses have sophisticated analytical techniques for determining the amount of leverage that would be optimum for any given capital budget; government does not. Government has a single unified budget that appears to be an all-expense/no-investments budget. It is easy for the casual observer to falsely conclude that borrowing to fund any portion of it would be out of the question.

We do not draw this analogy to suggest that government adopt more sophisticated capital budgeting techniques. Doing so would misdirect policy-making energy and invite legislative mischief. Rather, we do it to show a two-step approach for getting out of the debt phobia box.

- We admit to ourselves that some of the spending in any budget will yield future benefits: fixing Social Security, providing the private sector with more financial power, and preventing war are three obvious examples.

- We admit that borrowing money to help fund good investments is not only harmless, but desirable and that maintaining a unified budget while treating tax reform and Social Security repair as capital-like expenditures is quite feasible.

Successful, growing businesses, experienced in utilizing borrowed money, know that four basic tenets govern the use of debt:

- Borrowing money for good investments is perfectly sound financial practice.

- Refusing to borrow at all, even when opportunities emerge, means missing some or all of those opportunities.

- “Unborrowing”—not just refusing to borrow for the future, but using surpluses from current operations to eliminate past borrowings—is a pessimistic, contractionary financial practice.

- Borrowing for bad investments or to keep current operations afloat, is a wasteful, risky financial practice.

Policy Choice 1: Debt Retirement

This is the national equivalent of unborrowing. Businesses using this option usually have lost confidence in their future and are using surpluses from current operations to liquidate past loans. Economist Jane Jacobs wrote that, in the macroeconomic sense, “The embarrassment of riches in an economy that is economizing on development of new work is temporary. It is a prelude to stagnation.” This policy option is the extreme result of a debt phobia.

Policy Choice 2: Balanced Budget

This choice means refusing to borrow, even to take advantage of bright opportunities. Although this is a less pessimistic policy than debt retirement, it is still debt phobic when there are lucrative purposes to which new borrowing can be put. It can be deceptive, because a modest level of economic growth can mask the missed opportunities for even greater wealth creation.

In a growing economy, a balanced-budget fiscal policy, which holds the nominal debt constant, produces automatic and gradual reduction in the debt burden; the numerator in the debt-to-output ratio remains constant while the denominator increases. But in spite of the shrinking debt burden, a balanced-budget fiscal policy will prove to be sub-optimal if it forces the government to pass up high-yield endeavors out of a fear of borrowing the necessary funds.

That said, a balanced-budget fiscal policy does allow for the tax revenue that otherwise would be used for debt retirement to be reallocated to higher-return endeavors such as tax rate reductions and limited personal retirement accounts. Thus, if surpluses were completely liquidated by reducing marginal tax rates, the balanced-budget fiscal policy that results would be more pro-growth than the debt retirement policy it replaced. Returning surplus revenues to the private sector via tax rate reductions would allow American business to invest those surpluses in ways that would raise productivity to improve long-run growth.

Policy Choice 3: Debt-Burden Neutrality

This choice means borrowing to invest in the future and limiting the quantity of borrowing to that justified by the performance of past and current investments.

Successful investments sooner or later have a beneficial effect on gross domestic product; unsuccessful ones do not. Our recommendation for maximizing economic growth is to identify high-yield structural reforms to government, establish a targeted range for the debt burden—the ratio of debt to GDP—then manage the budget so the debt does not (1) fall below the target into the stunted growth area or (2) rise above the target into the debt-burden-growth area (explained below).

Debt-burden neutrality entails allowing the nominal debt to grow incrementally each year to keep the debt-to-GDP ratio in bounds, while investing the proceeds in growth-enhancing reforms. As long as inflation remains under control and the debt burden is small enough not to create economic distortions or dislocations (which most economists agree is certainly the case with debt beneath 50 percent of GDP), the national debt can be permitted to grow annually in nominal terms without increasing the debt burden.

This debt-burden neutral fiscal policy maximizes growth because it maintains a steady debt burden that would permit the federal government to make long-term investments in long-term structural reform.20 No doubt lenders would willingly invest in a new tax code and a new Social Security system designed to fuel the economy’s growth engine.21

Conservatives may object to a debt-burden neutral fiscal policy on the ground that it opens the door to spending on inefficient and wasteful projects and programs. This can be a risk, but raising the specter of deficits when the real objection is to increased government spending is both dishonest political dialogue and ineffective political strategy. It is the strategy that gave rise to the Washington Stalemate in the first place and the highest level of taxation in American history.

Nevertheless, we agree that before embarking on intentional new borrowing that it would be prudent for Congress to adopt procedures that require tax rate reductions when the debt-to-GDP ratio falls below bounds unless increased government spending is demonstrably more productive than leaving the resources in the private sector.22 In other words, it is time to reverse the pay-as-you-go (“pay-go”) rules of the 1990s, which continue to bias congressional deliberations toward tax increases, and replace them with grow-as-you-go (“grow-go”) rules that allow prudent new borrowing.

Policy “Choice” 4: Debt Burden Growth

This needs little explanation. Few if any would recommend that the government assume a growing debt burden. In the private sector, any banker who sees a loan request that would result in a too-high debt-to-income or debt-to-assets ratio tends to view such a loan as too risky. The same logic applies to public finance: if past “investments” are not delivering sufficient GDP growth, fiscal policy has wandered outside the bounds of prudence.

Again, however, this is precisely the long-run fiscal strategy implicit in the conventional wisdom of retiring the debt today and foregoing important reforms so we can borrow more tomorrow to fund Social Security’s day-to-day operations. Such a policy is the antithesis of fiscal discipline.

Congressional and presidential spending behavior during both deficit and surplus years offers evidence that deficits may place an upper bound on how much the government can spend, whereas huge persistent surpluses leave spending increases open-ended. As we will see below, if a debt-burden neutral deficit is used to finance a reduction of the average tax burden to the neighborhood of 16.5 percent of GDP in 2008, spending would be constrained to go no higher than 18 percent of GDP without driving the deficit out of the “safe zone.” Both spending levels and tax receipts could grow in tandem with a faster-growing GDP.

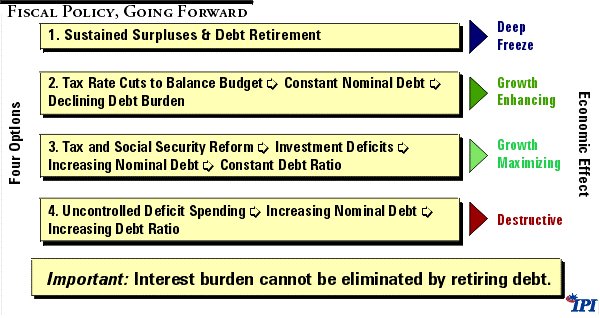

Our Recommendation: The Growth-Maximizing Policy

Figure 6 lays out four basic fiscal options for comparison.

Figure 6

Again, under current circumstances we recommend Policy Choice 3: Debt-Burden Neutrality. The escape from the austerity trap comes through using debt and financial leverage as the means of changing government policies that damage the economic welfare of the nation.

To achieve its full potential, our nation must find the courage to reject debt phobia and adopt an attitude of optimism, of faith in the future. We should direct our energy towards deciding what are the right things to do; we should stop wasting energy worrying about borrowing money to do them. If they are the right things to do, they will increase our ability to support the modest, necessary higher level of debt. A targeted debt-to-GDP range will allow us to stride a middle path between uncontrolled deficits and deep-freeze stagnation.

The Payoff of Maximizing Economic Growth

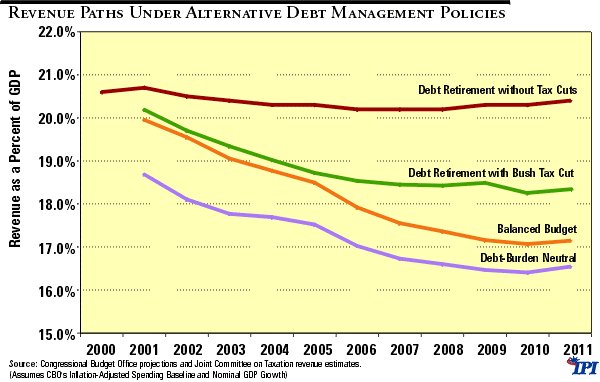

Political considerations aside, the economic arguments for borrowing money to finance major reforms are compelling. Figure 7 uses short-run static estimating techniques to compare the levels of revenue produced by Options 1–3. 23

Figure 7

Note that on a static basis, the Bush tax-cut proposal falls between the deep-freeze and growth-friendly revenue paths but leaves the average tax rate substantially above the rate achievable under a debt-burden neutral fiscal policy or even a balanced budget. According to CBO data, if the federal government began running a balanced budget today and allowed economic growth to shrink the debt burden automatically, spending of about 17 percent of GDP in 2010 would cover all entitlement obligations under current law (including Social Security benefits), discretionary spending increases for inflation and debt service payments. This means it would still be possible to practically double President Bush’ ;s tax rate reduction beyond 2005 even though it would be necessary to continue paying the debt service eliminated by debt retirement under the smaller Bush tax cuts. In 2010, federal revenues could decline from slightly more than 18 percent of GDP to 17 percent of GDP, and the debt would still fall below 23 percent of GDP.

Assuming interest rates remain constant, nominal debt service payments remain fixed each year under a balanced budget. If the operational side of government spending does not increase as a share of national output, overall government spending will fall as a share of GDP. Alternatively under a balanced budget, the operational side of government may actually grow larger over time even while recorded overall spending remains a constant share of GDP if an increase in non-interest spending is allowed to replace the declining share comprised of debt service payments. By contrast, under a debt-burden neutral fiscal policy, nominal debt service payments increase annually but remain a constant share of GDP, as will overall spending if non-interest spending also remains a fixed share of output. Therefore, because debt-service payments will be higher at the end of year 10 under a debt-burden neutral fiscal policy, overall spending will be higher as a share of GDP than it would be with a balanced budget, other things equal. Under current CBO baselines, spending would amount to about 18 percent of GDP in 2011 if nominal debt is allowed to grow in the interim at the rate of nominal output.

With nominal GDP growing annually at 5.0 percent (the CBO assumption), the implied debt-burden neutral deficit would equal 1.6 percent of GDP in 2011. [See Appendix Table A-2] Therefore, if Congress and the president went for the recommended growth-maximizing option and sought to maintain the nation’s debt burden within a targeted “safe zone,” it would be possible to overhaul the tax system and lower tax rates sufficiently to reduce the federal tax bite from slightly more than 18 percent of GDP to about 16.4 percent of GDP. This would allow workers to put 4.0 percentage points of the payroll tax (1.6 percent of GDP) into personal retirement accounts.24 The revenue shortfall (1.6 percent of GDP) created by diverting 4.0 percentage points of the payroll tax into personal retirement accounts could be covered by borrowing without violating the debt-burden-neutrality constraint.

The National Debt and Tax Reform

There’s more good news. The comparisons above are all based on the unrealistic static assumption that tax rate reductions and fundamental tax reform would have no salutary effect on economic performance. In fact, there is strong evidence that they would significantly enhance the economy’s performance and raise the long-term growth rate.25

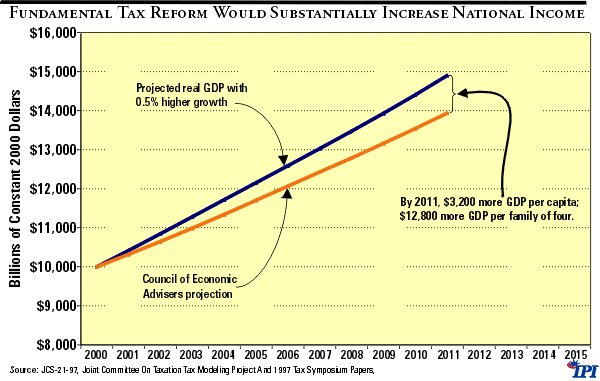

Based upon the research findings of Fiscal Associates, an economics consulting firm located in Arlington, VA, if tax reform lowered the top marginal income tax rate to 17 percent and eliminated the multiple taxation of saving and investment, Americans could expect the real rate of economic growth to rise by a full percentage point during the first three to five years and then remain a half-point higher thereafter. This effect is illustrated in Figure 8.

Figure 8

As a result of this added growth, the magnitude of the “revenue loss” produced by the reforms would likely be at least a third less than indicated by static estimates and would be more than recouped over the long run.26

If policy makers would adopt a debt-burden-neutrality criterion and free themselves of the mindless constraint of revenue neutrality, they could effect fundamental tax reform quite soon. They could replace the current tax system with one that prescribes one or two low rates for all taxpayers. In so doing, they could provide relief for working Americans; protect taxpayer rights; halt collection abuses; end bias against work, saving and investing; promote economic growth and job creation; and impose rules to ensure substantial consensus before taxes are raised.

Every additional dollar of tax revenue raised through the current tax code retards and damages the economy far more than can be offset by using that revenue dollar to retire public debt. Indeed, the current tax code is so economically destructive that for every additional dollar in tax revenue raised, economists estimate that overall GDP is reduced by from $1.20 to $1.60. 27 Even without considering that the rate of return on the private investment of the surpluses would exceed the rate of interest due on the public debt, the cost of raising the surplus revenues through the current tax code would make debt retirement the fiscal equivalent of taking three steps back for every two forward.

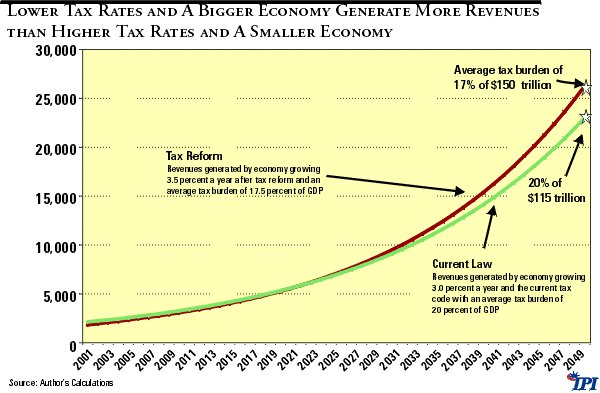

At a minimum, it makes more sense to cut tax rates, balance the budget and return all of the budget surpluses to taxpayers than it does to employ the current tax code to raise the surpluses necessary to retire the public debt, which comes at the expense of stifling saving, shrinking investment and retarding economic growth. Long-term thinkers would go further than that and conclude that this is the ideal time to finance a complete overhaul of the tax system. Figure 9 illustrates the long-run revenue consequences of cutting marginal tax rates to no more than 17 percent and properly redefining the tax base.

Figure 9

The National Debt and Social Security

One unpleasant fact cannot be ignored: with the ratio of workers to retirees at roughly three-to-one and falling, demographics make the existing Social Security program obsolete. Policy makers must soon acknowledge that payroll taxes would have to rise above 18 percent to salvage the program. The economy could not tolerate this level of taxation and perform as it has for the past decade. Moreover, giving up economic growth and standard-of-living increases would do nothing to improve the average 2 percent—and falling—rate of return that workers receive on their payroll taxes.

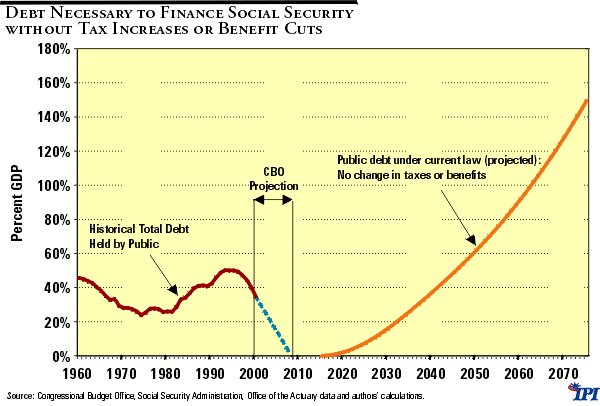

During the 2000 presidential campaign, Vice President Al Gore echoed Senator Daniel Patrick Moynihan when he averred that Social Security is sound and could be saved through programmatic reform and retirement of the national debt. The vice president and the Senator, like many policy makers, ignored the fact that unless we transform Social Security into a true investment program, we will have to raise payroll taxes beyond workers’ ability to pay them, or we will have to borrow vast sums.

Figure 10 uses Social Security Administration projections to extrapolate the magnitude of public borrowing that would be required to maintain current benefits under the existing program without increasing tax rates on workers or retirees. By 2075, the national debt would amount to almost 150 percent of GDP. In present value terms (in today’s dollars), that debt amounts to almost $13 trillion.

Figure 10

The economically rational thing to do is to recognize the transition costs of moving to a personal-accounts-based retirement system as a capital-like expense and begin steady and measured borrowing now to make the investment.

In order to examine the full potential of implementing a debt-neutral fiscal policy to effect these major structural reforms, we relaxed the unrealistic static assumptions above and simulated the long-run dynamic effects of a combined tax-reform/Social Security reform package using the Fiscal Associates macroeconomic model and Social Security calculator. Recall, the FA model projects that if the top marginal tax rate were lowered to 17 percent and the federal tax base were redefined to eliminate multiple taxation of saving and investment and other distortions, the long-term real economic growth rate would rise by 0.5 percent a year after a five-year adjustment period of even higher annual growth.28 CBO currently assumes a long-run real annual growth rate of 3.1 percent, which implies a post-tax-reform growth rate of 3.6 percent.

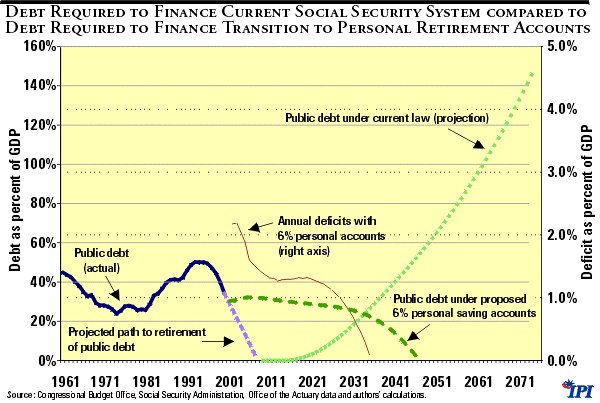

With tax reform of this magnitude, workers could immediately place 6 percentage points of the payroll tax into personal retirement accounts, the government could safely borrow the transition costs each year (amounting to average annual borrowing of 1.2 percent of GDP between now and 2035), and the nation could keep its debt burden within a few percentage points of today’s level for the next 25 years, after which it would begin to fall precipitously. According to the FA model, by 2025 federal revenues generated by lower rates and a reformed tax code would exceed the amount of revenues that today’s tax code would produce with higher rates, and the return on the private retirement accounts by then would have mounted sufficiently that overall retirement income would rise by almost one-third while federal outlays would decline significantly. Before mid-century, growth-induced budget surpluses would emerge once again. In present value terms, the transition borrowing cost of moving to private retirement accounts financed by 6 percentage points of the payroll tax would amount to only $1.6 trillion, about one-ninth of the debt burden confronting us if we simply attempt to patch up Social Security.

Figure 11 compares the amount of debt that will be required to finance Social Security as it is currently structured to the amount of debt required to finance the transition to a universal system of personal retirement accounts. The thin solid line measured on the right axis is the annual borrowing requirement.

Figure 11

During the transition period, the IOUs held in the so-called Social Security Trust Fund would be redeemed by the Treasury with money borrowed from the public. The proceeds would be used to cover the revenue shortfall that would arise as workers invested their payroll taxes in personal retirement accounts. Indeed, since workers likely would invest part of their retirement funds in federal bonds, the shortfall in payroll taxes could be made up by borrowing funds directly from the personal accounts. The effect would be to transfer the Social Security Trust Fund “assets” to the public, where they belong.

Said another way, since its inception, many citizens have perceived Social Security to be a retirement savings fund; so far, that has been a false perception. However, this plan would turn that perception into reality with no adverse effect on benefits.

A Final History Lesson: England’s Public Debt Saga

The saga of England’s “gigantic, fabulous” public debt illustrates the benefits of using and managing public debt in a manner both aggressive and prudent. England financed the bulk of its great public debt throughout the 18th Century through perpetual debt instruments called Consols at very low interest rates (so-called Three Percents). As discussed above, a stable government like that of Britain or the United States can borrow without having to repay the principal because, unlike an individual’s, a nation’s future income stream lives on in perpetuity.

Thomas Macaulay’s History of England, written in the mid-19th Century recounts the now-familiar misconceptions about the burden of public debt and sums up the fallacy of rushing to retire it:

Those who uttered and those who believed that long succession of despairing predictions erroneously imagined that there was an exact analogy between the case of an individual who is in debt to another individual and the case of a society which is in debt to part of itself; and this analogy led them into endless mistakes….They were under an error not less serious touching the resources of the country. They made no allowance for the effect produced by the incessant progress of every experimental science, and by the incessant effort of every man to get on in life. They saw that the debt grew and they forgot that other things grew as well as the debt.29

USA’s Debt Retirement Attempts since 1776: Ominous Results

Directly or indirectly, most Americans now own Treasury bonds. All told, the public owns $3.4 trillion worth of them. A few people own them outright; most have savings accounts, insurance policies or retirement funds backed by Treasuries. Mutual funds, for example, own about 7 percent of all outstanding Treasuries.30 Debt reduction eliminates those securities in what is effectively a bond fire.

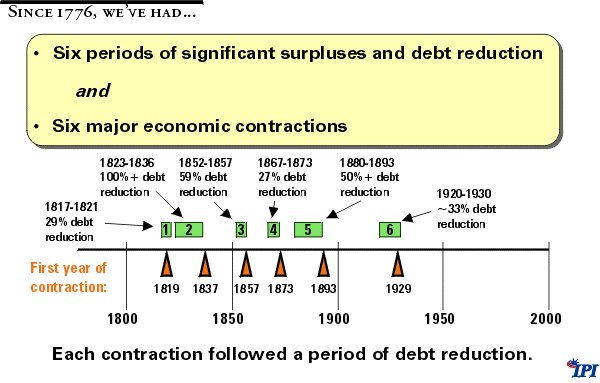

U.S. history presents many examples of the economic dangers that arise when the federal government undertakes to rapidly retire the national debt. Since 1776, there have been six periods of significant surpluses and debt reduction in United States. Each has been followed by a period of substantial economic contraction. That we have entered a seventh period of major debt reduction is ominous.

Figure 12

Conclusion

“

- If American conservatism can come to terms with the meaning of debt, it will represent a nearly unprecedented intellectual triumph.” – George Gilder, Wealth and Poverty

So let’s cancel the bond fire and go for growth. If that requires a modicum of borrowing each year, beginning now, let’s do it. “It will be to us [and to our children and their children] a national blessing.”

Endnotes

i Macaulay, Thomas, History of England, as quoted in George Gilder, Wealth and Poverty , Institute for Contemporary Studies, San Francisco, Calif., 1981.

ii The Debt and the Deficit: False Alarms/Real Possibilities, Robert Heilbroner and Peter Bernstein, W.W. Norton & Co., New York, 1989, pp. 27 and 138.

iii Ibid.

iv Radio Address, July 27, 1979. It is contained in Reagan In His Own Hand, Edited by Kiron K. Skinner, Annelise Anderson and Martin Anderson, The Free Press, New York, 2001, p.283.

1 By about 2008, according to the Congressional Budget Office. See The Budget and Economic Outlook: Fiscal Years 2002-2011 , January 2001, Table 1-4.

2 “Continuing to run surpluses beyond the point at which we reach zero or near-zero federal debt brings to center stage the critical longer-term fiscal policy issue of whether the federal government should accumulate large quantities of private (more technically nonfederal) assets. At zero debt, the continuing unified budget surpluses currently projected imply a major accumulation of private assets by the federal government. I believe…that the federal government should eschew private asset accumulation because it would be exceptionally difficult to insulate the government’s investment decisions from political pressures. Thus, over time, having the federal government hold significant amounts of private assets would risk sub-optimal performance by our capital markets, diminished economic efficiency, and lower overall standards of living than would be achieved otherwise.

3 “Assuming the Treasury begins to invest surpluses in the stock market as soon as it has retired all the debt that it can and that these investments earn a 10 percent annual return, our government could be sitting on a stock-market portfolio worth about $20 trillion in twenty years…Projecting forward, the U.S. government could own about one-fifth of all domestic equities.” See Kevin A. Hassett, “Putting Our Tax House in Order,” American Enterprise Institute for Public Policy Research, March 2001.

4 “Private asset accumulation may be forced upon us well short of reaching zero debt. Obviously, savings bonds and state and local government series bonds are not readily redeemable before maturity. But the more important issue is the potentially rising cost of retiring marketable Treasury debt. While shorter-term marketable securities could be allowed to run off as they mature, longer-term issues would have to be retired before maturity through debt buybacks. The magnitudes are large: As of January 1, for example, there was in excess of three-quarters of a trillion dollars in outstanding nonmarketable securities, such as savings bonds and state and local series issues, and marketable securities (excluding those held by the Federal Reserve) that do not mature and could not be called before 2011. Some holders of long-term Treasury securities may be reluctant to give them up, especially those who highly value the risk-free status of those issues. Inducing such holders, including foreign holders, to willingly offer to sell their securities prior to maturity could require paying premiums that far exceed any realistic value of retiring the deb t before maturity.” Greenspan, op..cit.

5 A Blueprint for New Beginnings: A Responsible Budget for America’s Priorities, Office of Management and Budget, Washington, DC, 2001, p. 12.

6 “Eliminating unified surpluses by transforming social security into a defined-contribution system with accounts held in the private sector would likely better maintain national saving levels. But the nature of social security would at the same time be fundamentally changed. Alternatively, unified surpluses could be used to establish mandated individual retirement accounts outside the social security system, also mitigating the erosion in national saving.” See, Testimony of Alan Greenspan, before the Committee on the Budget, U.S. House of Representatives, March 2, 2001.

7 Greenspan, op.cit, January, 2001.

8 “If, for example, the accumulation of assets is avoided by eliminating unified budget surpluses through tax and spending changes, public and presumably national saving may well fall from already low levels.” Greenspan, op.cit, March, 2001.

9 Phillips Curve theory holds that there is a trade-off between inflation and unemployment.

10 Keynes, John Maynard, The General Theory of Employment, Interest, and Money , Harcourt Brace & Co., San Diego, 1964, pp. 94-95.

11 For a review of the literature, see Richard W. Rahn and Harrison W. Fox,Jr., “What Is the Optimum Size of Government?” Vernon K. Krieble Foundation, September, 1996. See also Gerald W. Scully, “Measuring the Burden of High Taxes,” Policy Report # 215, National Center for Policy Analysis, Dallas, July 1998. Additional recent research on the topic can be found at the Web site of the Joint Economic Committee, www.house.gov/jec/.

12 Unlike the Keynesian demand-side model, which holds that deficits have a direct stimulative effect on the economy by increasing aggregate demand, deficits are viewed in the supply-side model as perhaps necessary but not inevitable in the short run. Both politics and economics may require deficits to facilitate reductions in tax rates that increase the after-tax rate of return to work, saving and investment, lead to more of all three and generate higher revenues from a larger economy at lower tax rates.

13 See Lawrence A. Hunter, “On the Origins and Persistence of Federal Budget Deficits since 1980,” Policy Report # 141, Institute for Policy Innovation, Lewisville, Texas, June 1997.

14 Kemp, Jack, Advancing the American Idea in the 90’s , Campaign for A New Majority State, p. 105.

15 In fact, there is good reason to believe that the “official” budget surplus estimates of CBO and OMB are considerably underestimated. CBO, for example, projects that revenues on average will grow more slowly than the economy during the coming decade; that is historically unprecedented. Since 1963, including three major economic recessions, revenue has grown 1.04 percent for each 1 percent growth in the economy. Since the 1986 tax reform act, revenues have grown on average 18 percent faster than nominal GDP. Since 1993, revenues have grown on average 37 percent faster than nominal GDP. If revenue growth is assumed to be no greater than its long-term, pre-tax rate reduction pace, projected surpluses would go up by $775 billion during the coming decade; if revenues are assumed to grow on average 18 percent faster than nominal GDP, as they have since 1986, projected surpluses would be $2.1 trillion larger, or $7.7 trillion, between 2001 and 2011.

16 Since 1997, Congress has spent $83 billion above and beyond the so-called budget caps put in place by the “balanced budget” act. Since 1998, total discretionary spending has increased 16 percent and nondefense discretionary spending has increased 20 percent.

17 “The Additional Needs and Contingency Reserve is ultimately an insurance policy. For example, budget surpluses may not be as large as currently projected, farm conditions could require additional resources for agriculture, and more money may be needed for national security requirements.” “ Overview of the President’s 10-Year Budget Plan, A Blueprint for New Beginnings, Washington, D.C,. 2001, pp. 12-13.

18 www.amazon.com book review.

19 If tax rates are cut enough to extinguish surpluses in the short run and balance the budget, eventually the larger GDP produced by the improved incentives to produce will generate even more revenue at lower rates, and surpluses will reemerge. Until tax rates are reduced to the point at which economic output is maximized, tax rate reductions designed to extinguish surpluses over the short run will cause economic output and revenues to rise enough to generate new surpluses and justify further tax rate reductions.

20 Not because the act of deficit finance itself has any intrinsic value i.e., a “multiplier effect” on aggregate demand.

21 If the national debt grows at the same rate as the economy, that is, if the government runs annual deficits equal to the rate of economic expansion multiplied by the existing nominal debt total, the nominal value of the national debt will grow each year by the amount of the deficit but, the debt-to-GDP ratio will remain constant. and the debt burden will not grow. If annual deficits equal less than the economy’s growth rate times the current debt, nominal debt will grow but the debt-to-GDP ratio will decline more slowly than if the nominal debt is held constant. [See Appendix Table A-2]

For example, with GDP at $10 trillion and the current national debt at $3,400 billion, if nominal GDP is expected to grow by an average of 5.0 percent a year well into the future, as the Congressional Budget Office forecasts, the government can run an annual budget deficit of about 1.5 percent of GDP (0.05 x $3, 409 = $170 billion in 2001) without increasing the debt burden. In 2001, spending is expected to amount to 18 percent of GDP, which means tax rates could be cut immediately down from their current level of 20.7 percent to 16.5 percent of GDP without increasing the burden of the national debt.

22 Another frequent objection to deficits is the claim that they are inflationary. Deficits may indeed be inflationary but they need not necessarily be so. It is not the act of borrowing by the government per se that is inflationary but rather excessive monetization of the debt by the central bank. Deficits will be inflationary only if the central bank becomes a co-conspirator to deficit spending by monetizing more of the national debt (i.e., purchasing more of the government’s debt held by the public) than is required in its legitimate conduct of open-market operations to supply markets the liquidity they demand. When the central bank purchases government debt from the private sector it holds the debt in its portfolio but returns the interest payments to the Treasury, thus reducing the financial burden the debt places on the government. But in purchasing the debt from the private sector, the central bank injects new money into the economy, which will be inflationary to the extent that it exceeds the amount of new money (liquidity) demanded by a growing economy. The inflation is reflected in the elevated nominal GDP caused by price level increases over and above the real GDP increases due to higher production. When the central bank becomes a co-conspirator to deficit finance, the debt burden is literally inflated away as the denominator of the debt-to-GDP ratio (i.e., nominal GDP) is artificially increased, causing the debt-burden ratio to measure artificially small. If the central bank refuses to monetize more of the national debt than it is legitimately required to in its conduct of monetary policy, deficits and the national debt will not be inflationary. Nevertheless, the deficit spending will be inefficient to the extent of the opportunity costs, i.e., to the extent that real GDP is lower due to funds being put to public purposes less productive than the private uses to which they could have been put had they not been borrowed away by the government. Thus, it is the spending occasioned by the deficits rather than the deficits per se that is inefficient. To see that it is the spending rather than the choice of deficits to finance it that is inefficient, consider the fact that were the same ill-considered spending tax financed rather than deficit financed, the economy would suffer not only the opportunity costs generated by inefficient public spending but also the “extraction costs,” or dead-weight loss produced by extracting tax revenues from the private sector.

23 Revenue paths assume CBO nominal GDP growth projections, and add back interest payments and so-called “proceeds earned on the balance of uncommitted funds” (expressed as “negative outlays”) to CBO’s inflation-adjusted spending baseline in the cases of the Balanced-Budget and debt-burden neutral policies. CBO’s accounting exercise of assuming the government earns an increasing return on its investment of accumulated budget surpluses after the national debt is retired (rising from 3.6% in 2006 to 4.6% in 2011) takes single entry bookkeeping to a new extreme. By 2011, under CBO’s “primative Keynesian” economic model, continuing to run enormous budget surpluses after the national debt is retired and investing them in the private sector allows the federal government to accumulate almost 20 percent of annual GDP in private assets that are yielding an increasing return each year without affecting economic growth.

24 Taxable payroll under Social Security is projected to average about 40 percent of GDP.

25 JCS-21-97, Joint Committee On Taxation Tax Modeling Project And 1997 Tax Symposium Papers,

26 In his evaluation of the Reagan tax rate reductions, Lawrence Lindsey concluded that they “cost less than one-third as much as implied by the naively calculated direct effect or static estimate… In 1982 this true revenue cost amounted to only $6.1 billion, compared to the $44 billion direct effect estimate. By 1985, the true revenue cost had grown to $33 billion as compared to the direct effect estimate for that year of $114.9 billion.” See Lawrence B. Lindsey, The Growth Experiment , Basic Books, Inc., New York, 1990, pp. 74–76.

With respect to the Bush tax-cut proposal, Harvard economist and National Bureau of Economic Research head Martin Feldstein, testified recently before the Ways and Means Committee of the US House of Representatives that “ …the true cost of reducing the tax rates is substantially smaller than the costs projected in the official estimate. Studies of past tax rate reductions show that taxpayers respond to lower marginal tax rates in various ways that increase their taxable income. They work more and harder and take more of their compensation in taxable form and less in fringe benefits.

“At the National Bureau of Economic Research, we have used a large publicly available sample of anonymous tax returns provided by the Treasury to estimate how the actual revenue loss would compare to the official estimates that ignore most of these behavioral responses. Our analysis shows that when the proposed Bush tax cuts are fully phased in, the net revenue loss would be only about 65 percent, only about two-thirds, of the officially estimated costs.